In What Ways Has Increased Availability of Leisure Time Affected the Fashion Market?

Contrary to conventional wisdom, there's been no central rewiring of the consumer. The modern consumer is a construct of growing economic pressure level and increasing competitive options.

The consumer is changing. They are more capricious and less loyal. They have less time but are more conscientious. They shy away from stores and adopt experiences over products. Today's consumer is an entirely unlike animal—and unrecognizable from their peer from the adept old days. This brand of conventional wisdoms has been proliferating in the market for a few years now. It appears as if there has been a seismic shift in the consumer's mindset—and choices—a shift that has left the market asking: "Who is this brand-new consumer?"

There are even more clichés surrounding the millennial consumer. They are ofttimes branded as being more narcissistic, more than idealistic, more socially-conscious, and more than experience-oriented than whatsoever of their preceding generations. They have even been blamed for ruining everything from movies to spousal relationship!i They seem to have broken the mold of their similar-aged cohorts of past eras.

Amid this disruptive and fast-changing narrative nigh the irresolute consumer, we paused to ask ourselves some hard-striking questions to cut through the noise and arrive at the truth. Has the consumer fundamentally changed? If yes, in what ways have they changed? Is at that place a seismic difference in the changes that we are witnessing? More importantly, is the hysteria in the market obscuring a much deeper and more key change in consumer behavior?

It is with these questions in heed that we conducted a year-long written report to go across the headlines and unearth more profound observations about the consumer that might have been either missed or misunderstood in the midst of the hype.

Our findings debunked many conventional wisdoms about the new-age consumer. What nosotros learned is that the consumer hasn't fundamentally changed, but to the extent they are irresolute is because the environs effectually them is evolving, characterized by economic constraints and new competitive options. They're irresolute because of the fiscal constraints they find themselves in. This, in turn, has been triggered by a ascension in nondiscretionary expenses such as health care and pedagogy and the growing bifurcation betwixt income groups. They're also changing in reaction to the abundance of competitive options available to them, made possible by engineering science.

It's this swirl of financial and marketplace dynamics that is heavily influencing the behavior of today'southward consumer as opposed to a fundamental rewiring.

Understanding the consumer: Our approach

We undertook a yearlong journeying to report the consumer. We scoured government information; talked to clients, industry leaders, and analysts; conducted chief interviews; and surveyed a representative sample of more than than 4,000 consumers from the United states. Working with Deloitte'south Center for Consumer Insights, nosotros conducted principal inquiry, leveraging 450 billion unique points of location data and more than 200 billion points of credit card transactions. Our goal was to examine the current state of the consumer as well every bit to study their beliefs and underlying attributes to meet if there were nuances and intricacies that were existence missed.

We adopted a two-pronged approach to our research.

Commencement, we zoomed out to study the macro demographic, cultural, and economic trends related to the United states consumer. Our focus here was non on behavior but on wide trends that impact beliefs. It'due south similar to the approach we took in an before study, The nifty retail bifurcation.2 In that, we looked at the income and expenditure data to examine whether and how the economic situation of consumers had changed and the implications of that alter. Simply this fourth dimension, we wanted to get deeper: We wanted to dig into other broad categories of demographics and regional changes to see where they alive, their ethnicity and race, and how factors such as economic state of affairs and health condition are driving changes in consumer behavior.

Second, we examined main information on the consumer'due south changing demographics and economics to understand consumer beliefs—non just their overall behavior simply their micro-behaviors, which differ, sometimes substantially, within emerging segments. We looked deeply at how they spend their money and time, where they get, and what'south most important to them.

In this report, nosotros have highlighted the most intriguing insights from our study to put together the construct of a consumer who in some means is changing and in other ways isn't really changing at all.

The changing consumer: Deconstructing demographic dynamics

A grasp of demographics is critical to understand what makes the world—and the consumer—tick. Nosotros are our demographics. This doesn't mean that the consumer tin exist reduced to the sum of their private demographic categories. It ways that they're a creation of the circuitous interplay of e'er-shifting demographic forces that create unique needs, cultural biases, and define consumer behaviors.

To sympathise how, where, and why the consumer is irresolute, one must understand their underlying demographics, which include much more than than just life span, fertility rate, race, and ethnicity. Wellness, culture, economic science, and educational activity are all critical dimensions of demographics—every bit are geography, regionalism, and the urban-suburban-rural divide. Understanding these changing demographics helps shine the light on any emerging pockets of opportunity.

Millennials are the virtually diverse generational accomplice in Us history.

A diversifying consumer base with diverse needs

At that place is a seismic shift that has taken place in the United States over the past 50 years. The population has become increasingly heterogeneous: Millennials, now representing 30 percent of the population, are the about diverse generational cohort in US history, with roughly 44 percentage consisting of ethnic and racial minorities. In comparing, only 25 percent of baby boomers belong to ethnic and racial minorities (figure 1).3

This increased diversity, while most pronounced in the millennial generation, is non a uniquely millennial attribute. The shift in the ethnic and racial makeup of the U.s. has been underway for some time at present, with the consumer base becoming increasingly diverse. The current racial makeup of the United States (and the consumer) is barely 50 percent white and the number is probable to go along shrinking.four The non-Hispanic white population is projected to driblet from 199 million in 2020 to 179 1000000 in 2060—a reject of x percent—even as the United states of america population continues to abound.v

This shows that we accept moved to a diverse, splintered, and heterogeneous consumer base with a much broader and varied set of demands and needs. Moreover, the upcoming Gen Z accomplice is likely to bring further diversification of the consumer base along racial and ethnic lines.

Young consumers are moving toward metropolis centers

The onetime axiom of politics, "All politics is local," is too applicable to consumer trends. Where the consumer lives—or their geography—further shapes their needs and demands.

For much of the late 19th and early on 20th century, Americans settled in cities in pursuit of factory piece of work. Following World State of war II, families fled cities to suburbs that epitomized the American Dream—a few kids, a domestic dog, and a business firm with a white lookout man fence that the working-class American could of a sudden afford.6 This demographic transformation radically changed the retail mural and the consumer.

The U.s. has moved to a more than diverse, heterogeneous consumer, with a much broader set of needs.

Looking at geographic data from 2000–2014, nosotros see that the trend of movement to the suburbs is all the same intact. Suburban life appears to be flourishing, with suburbs witnessing a net population growth and cities and rural areas seeing a turn down.7

Yet, inside this geographic information, gradations are beginning to appear, bringing with them farther splintering of the market. Rather than leaving urban centers (which was characteristic of the baby boomers), young consumers announced to have reversed class and are moving closer to the urban core—to city centers—mayhap drawn past proximity to work and cultural activities.

Now, to a degree, one tin can argue that this trend is function of the general pattern—that when the younger consumers finally do settle downwardly and showtime families, they volition follow in the footsteps of their predecessors and motility to the suburbs. However, the data shows a pregnant jump in the population growth rate of younger consumers in and around cities in the decade beginning 2010 (eighteen percent), as opposed to the failing growth charge per unit in the previous decade—2000–2009 (–4 per centum).8

This reverse trend of movement toward urban center centers is adding to the complication of the consumer landscape, just as the postwar migration to the suburbs significantly impacted power and the distribution of money in the mid-20th century. It'southward disquisitional to monitor these migratory patterns every bit they influence the consumer'due south decision-making and purchasing beliefs beyond a broad set of categories, from rent to personal care products.9

Regional migration is fragmenting the consumer base

Geography isn't simply urban vs. rural. There are also broader regional population trends at play—the move of people within the United States—which shape geographic markets. As the census population estimates bear witness, the migration of people from the Northeast and Midwest to the Southeast and to the West continues to be a trend.ten

However, one time you swoop below the surface and examine the internal migration trends through the lens of age, stark differences begin to emerge. Baby boomers (many now in retirement mode) are moving to Florida and Arizona, which claimed 8 of their tiptop 10 metro destinations; Gen Xers are relocating to Texas, where five of their top 10 metro destinations prevarication; and millennials are migrating to Colorado and Florida, which contain five of their acme x metro destinations.eleven

This trend is fragmenting the consumer base further, equally each age accomplice follows a unlike debarkation and migration pattern. It also ways that each generational accomplice brings its ain set of needs and demands to the region they drift to, farther amplifying the differences among consumers in diverse parts of the state. If you take these dissimilar lenses—race and ethnicity, urban vs. rural, and geography—in conjunction, it is increasingly evident that the consumer can't exist thought of in simple, generalized means. Instead, we need to await at them through a kaleidoscope of factors to create a more complete picture of the dynamic consumer.

The consumer is more educated, and is spending differently

We looked at other shifts as well—for instance, cultural influences—to understand ways in which the consumer has changed. Over the past twenty years, the percentage of the population with college degrees or higher has increased significantly, though non uniformly—white and black Americans with a college didactics have increased by 12 percent and Hispanics by 7 per centum.12

As a upshot, we're moving toward a more educated and knowledgeable consumer base with different spending patterns. All the same, the cost of education eats into discretionary funds, influencing how consumers spend their money on categories such as dress, food away from home, and furniture. 13

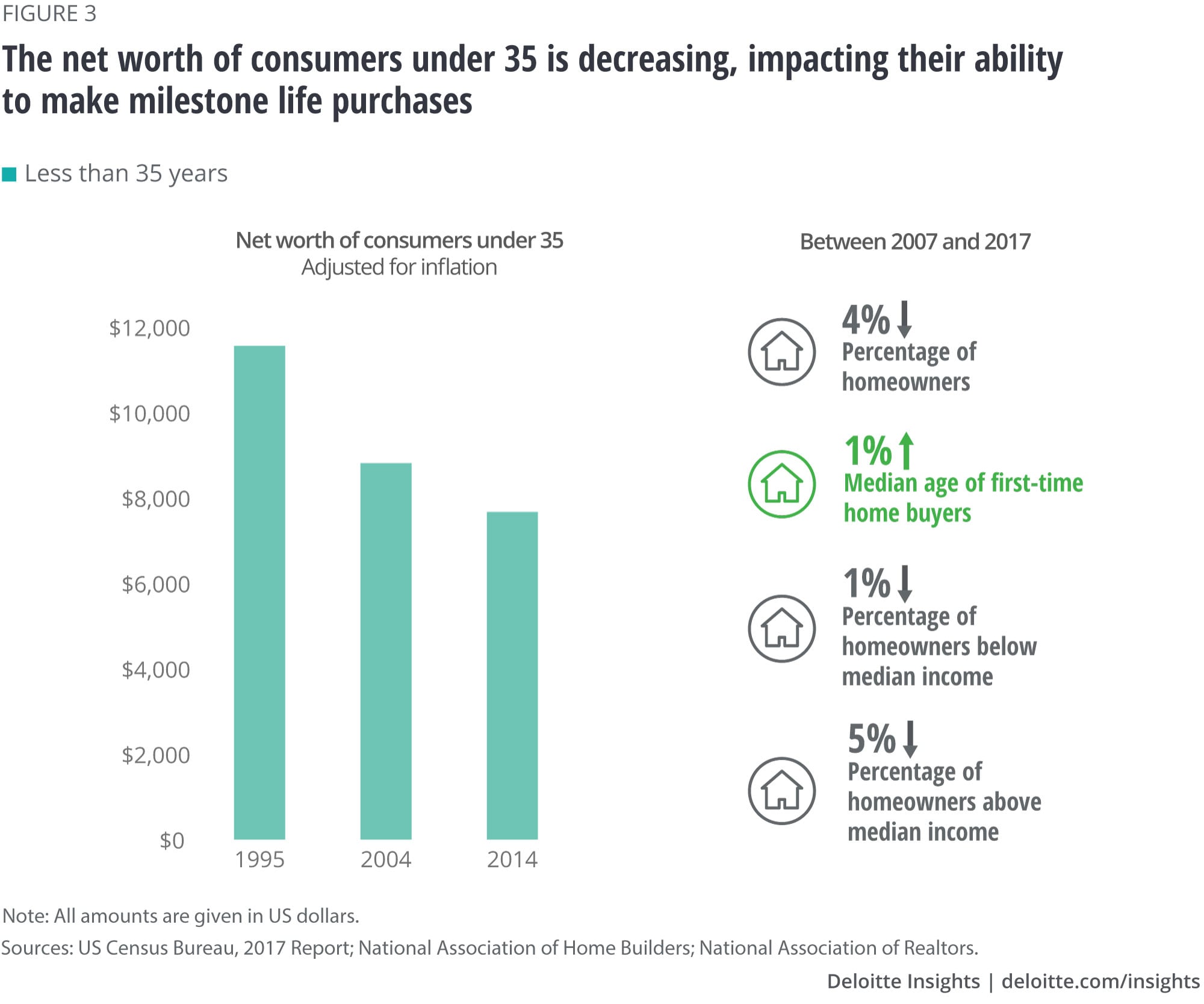

People are buying homes and getting married later—or never

Demographics, migration patterns, and education levels are not the merely factors evolving. Homeownership is a key life cycle milestone that also impacts consumer beliefs. In that location has been a marked drop in the percentage of consumers choosing to ain homes and many of them are waiting longer to buy homes. Between 2007 and 2017, the percentage of homeownership fell from 68 percent to 64 percent.14 Ane possible consequence of tougher lending standards could be the rise in the median historic period of first-time buyers to 32 years (from 31 at the start of the menses), an increase of 3 percent.15 Digging deeper into the median income figures of homeowners, we constitute that the percentage of owners with above-median income slipped to 78 percentage in 2017 from 83 percent in 2007, which suggests that homeownership is no longer an essential part of the American Dream.

Marriage, another life cycle milestone, continues to evolve. Between 1997 and 2017, marital rates among whites, Hispanics, and blacks fell from 59 percentage, 54 percentage, and 39 percent to 55 percent, 50 percent, and 35 percent respectively.xvi The simply exception to this down trend were Asians, whose marriage rate increased from 58 percent in 1997 to 61 per centum in 2017; the trend has been relatively steady since then.

Between 2007 and 2017, income growth for the high-income cohort rose 1,305 percent more than the lower-income group in the United States.

Not simply are fewer people marrying, they're besides delaying marriage: In a single generation, the median age of first union has risen from 26 to 28.5 years.17 The upshot of this delay ripples through various other life cycle milestones, such as an increase in the boilerplate age of women having their starting time children—up from 21 years in 1972 to 26 years in 2016.eighteen

These changes in cardinal life cycle milestones potentially influence how consumers spend their coin at retailers across categories equally spending takes place at after stages.

The economic carve up is deepening

In any discourse on the consumer, it would exist remiss not to mention their changing economical situation. As we starting time highlighted in The keen retail bifurcation,19 there is a deepening economical bifurcation between the top 20 percent income earners and the rest of the population—a split that has a huge impact on consumer behavior.

Between 2007 and 2017, income growth for the high-income cohort (>U.s.$100,000 in mean household income) rose i,305 percent more than the lower-income group (<U.s.$50,000 in hateful household income) in the U.s.. This divide has been even more conspicuous because of the ascent in nondiscretionary expenses across groups (figure 2). The bottom xl per centum of earners had less discretionary income in 2017 than they did 10 years ago, and the side by side 40 percentage saw only a modest increase. Only xx percent of consumers were meaningfully meliorate off in 2017 than they were in 2007, with precious little income left to spend on discretionary retail.

To make matters even more complex for retailers, new expenses and needs have arisen over the past decade that compete with traditional retail categories. These demands—such every bit for mobile phone and data plans—were minimal 10 years ago. So, traditional retailers have new contest for consumers' discretionary dollars.

This income gap has introduced precipitous distinctions between income categories as outlined in The corking retail bifurcation and the growing chasm is having a significant touch on on the consumer landscape.xx

Life expectancy is on the rise, merely so is obesity

On the positive side, life expectancy rates accept risen past ii.5 years on boilerplate, which ways people are living longer lives—but non necessarily healthier ones.21 The percent of people who are overweight or obese soared from 22 percent in 1994 to 42 percentage in 2016, nigh doubling.

So, there is a carve up in obesity rates likewise, with significantly lower obesity rates amid high-income consumers equally compared to the depression- and eye-income groups. Interestingly, fifty-fifty the high-income cohort saw the obesity rate ascension between 2007 and 2017, though more modestly than other income cohorts.

Inevitably, obesity impacts where consumers spend their money. An individual with a body mass index (BMI) that's considered "obese" spends 42 percent more on direct health care costs than adults who are a salubrious weight.22 These health care costs eat away at funds that may otherwise have been used on discretionary expenditure.

Are millennials losing economically?

The millennial has often been portrayed as a consumer who is at the epicenter of the disruption that'south taken place in every attribute of society, from marriage to childbearing to homeownership.23

Certainly, there are generational differences between this group and by cohorts: Millennials are meliorate educated and are marrying later, ownership homes later, and having children later on than the boomers did. But this trend is function of a broader one that'south been underway for decades.

Farther, blaming these changes in life bike milestones squarely on millennials ignores some not-historic period-related trends that are articulate in the data. Applying the lens of diversity on life cycle milestones reveals differences betwixt racial and ethnic groups. For example, among Asian millennials, first marriages are happening inside a narrow age band. In contrast, the distribution is much broader amid white, black, and Hispanic millennials.

Millennials are dramatically financially worse off than previous cohorts with a 34 percent decrease in their cyberspace worth since 1996.

Moreover, in that location'south a adept reason why millennials are reaching these milestones later in life: they are significantly financially worse off than previous like-aged cohorts. Since 1996, the net worth of consumers under the historic period of 35 has fallen by 34 percent.24 Homeownership for the cohort declined past more 4 percent between 2007 and 2017 (figure 3). And the rise in the pedagogy level of millennials hasn't come cheap: Between 2004 and 2017, educatee debt has increased for consumers under xxx past 160 percent. Typecasting the millennial as merely existence "unlike" overlooks a much bigger cistron—that of their economic constraints.

Companies oft say they demand to "win with the millennial." But the data nearly the economic well-being of this cohort shows that the millennial may well be losing economically.

To conclude, today's consumer—both millennial and nonmillennial—is not an entirely different species. Yet, they're operating in a new demographic, economic, and cultural landscape every bit described below:

- The consumer base is increasingly diverse. The current consumer base of operations has evolved in the cantankerous-currents of a set of broader demographic trends that have turned what was a homogeneous mass marketplace into a heterogeneous marketplace, consisting of multiple competitive options to choose from.

- Economically, the mod consumer is under greater financial pressures compared to the consumer of 30 years ago. This is particularly evident among low-income, center-income, and millennial consumers.

- Consumers are delaying key life cycle milestones. From marriage and homeownership to having children, these delayed milestones (peculiarly among millennials) take implications on consumer beliefs.

These demographic, economic, and cultural forces have created a market place that is fragmented. And the average consumer base is representative of increasingly diverse subsets of consumers with singled-out needs who have increasingly distinct competitive options to address those needs.

Beyond demographics: A deep dive into consumer behavior

Demographics by themselves do non tell the unabridged story. So, we looked securely at consumer behaviors. Specifically, we looked for changes or insights beyond four wide behavioral aspects of the consumer: How they spend money, how they occupy their time, where they become, and what matters to them.

In our analysis, we applied demographic and geographical lenses to see if there are, in fact, changes in modern consumer behavior every bit compared to the past, and how these changes measure up to marketplace axioms.

How are consumers spending their money?

Since 2005, full retail spending in the United states of america has risen by about xiii percent to effectually US$three trillion annually. The retail market has been growing and continues to expand. In fact, in 2017, retail grew a healthy 2.3 percent.25 However, per capita retail spending remained flat for the well-nigh part of the menses, meaning that population growth, rather than greater spending per person, was the primary driver of the increase in spending.26

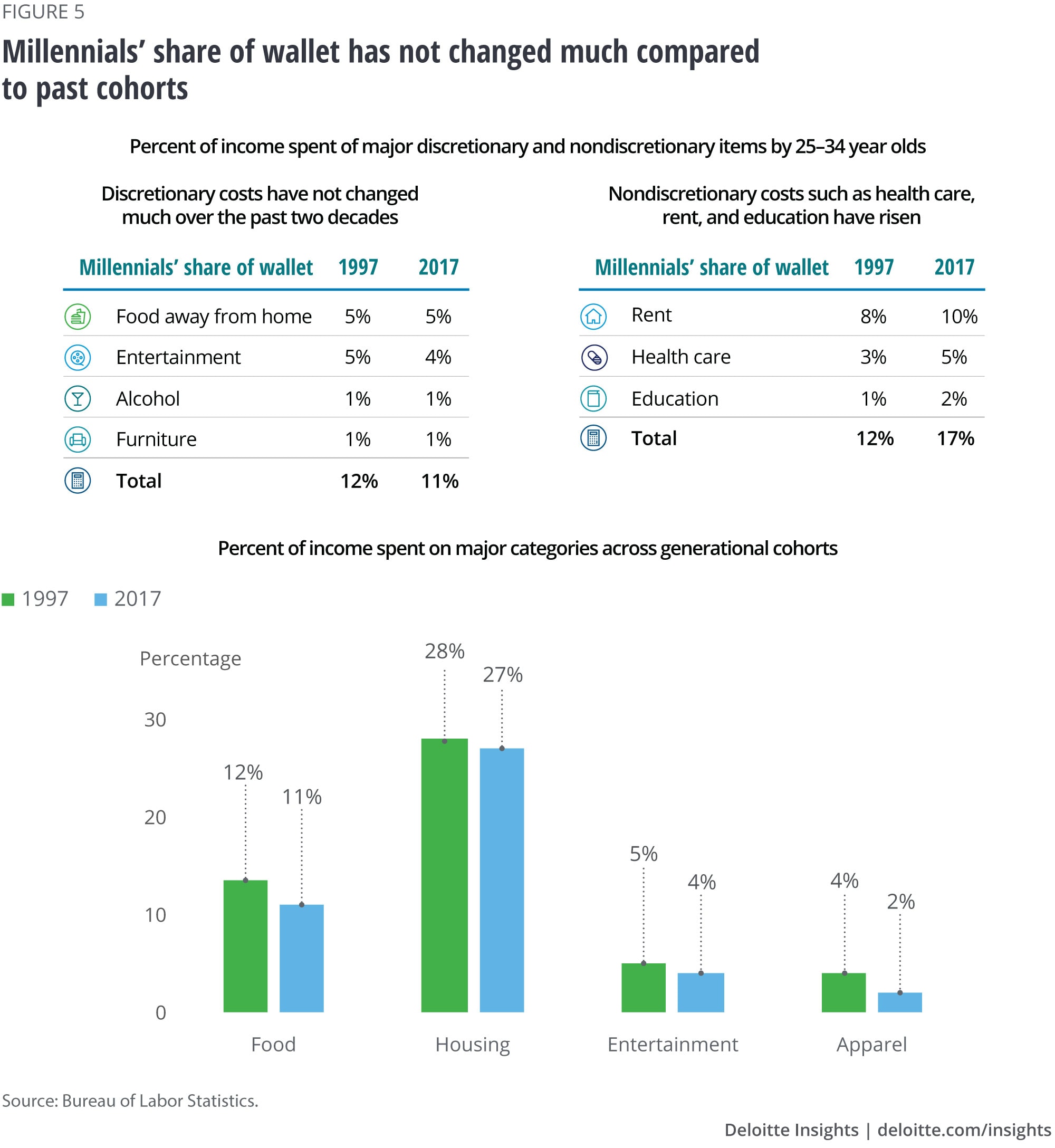

Also, surprisingly, the share of wallet data over a 20-year period reveals relatively consistent spending across nigh consumer categories. Food, booze, furniture, food away from home, and housing all found roughly the same pct of the consumer's wallet today equally they did in 1997. Even entertainment, a category where one might wait to see an increase in feel-driven spending, was basically flat. In fact, for consumers nether 30, spend on entertainment declined from 5 percent to 4 percent of the full wallet.27

The notable exception to stable consumer categories is apparel, where spending as a percentage of the total wallet has been cutting in half since 1987, declining from v percent to 2 per centum (figure 4).28 All the same, this abrupt drib does not necessarily imply a disinterest in wear or fashion on the role of the consumer.

Population growth has been the main driver of retail growth.

In fact, at that place has been a continued increase in the number of units of apparel sold, consequent with the overall rate of growth in retail.29 Farther, clothes spending by age cohort shows a similar phenomenon, with a similar decline in share of wallet in the category irrespective of age cohort. The data reveals a deeper story of deflationary pressures on clothes unit prices, with a significant downward trend in revenue per unit.30 It shows that the consumer is still buying wearing apparel at relatively robust levels. This trend is largely driven by changes in the competitive market place, with market forces driving down the price per unit.

But what about millennials? Is in that location a textile difference in their spending habits equally compared to those of similarly anile cohorts in the past? Afterwards all, the common perception is that they're the ones driving significant disruption. An analysis of spending patterns of similarly aged consumers over a 30-year menstruum reveals few significant shifts in spending allocation, with changes confined to a tight one percent to 2 per centum range (effigy 5). Interestingly, the real differences testify upwardly in several nondiscretionary expenditure categories. A growing share of the millennial's wallet is going toward wellness care expenses, housing costs, and instruction, highlighting non and then much a change in the consumer, simply rather a modify in the economical pressures that the young consumer is nether.

This ascertainment runs counter to conventional wisdom, which posits that millennials have shifted spending categories toward experiences and away from products. At that place is a nugget of truth in the popular idea, though. Loftier-income millennials are spending almost a third of their discretionary income on entertainment, and as their income levels rise, the absolute dollars spent on entertainment rise.

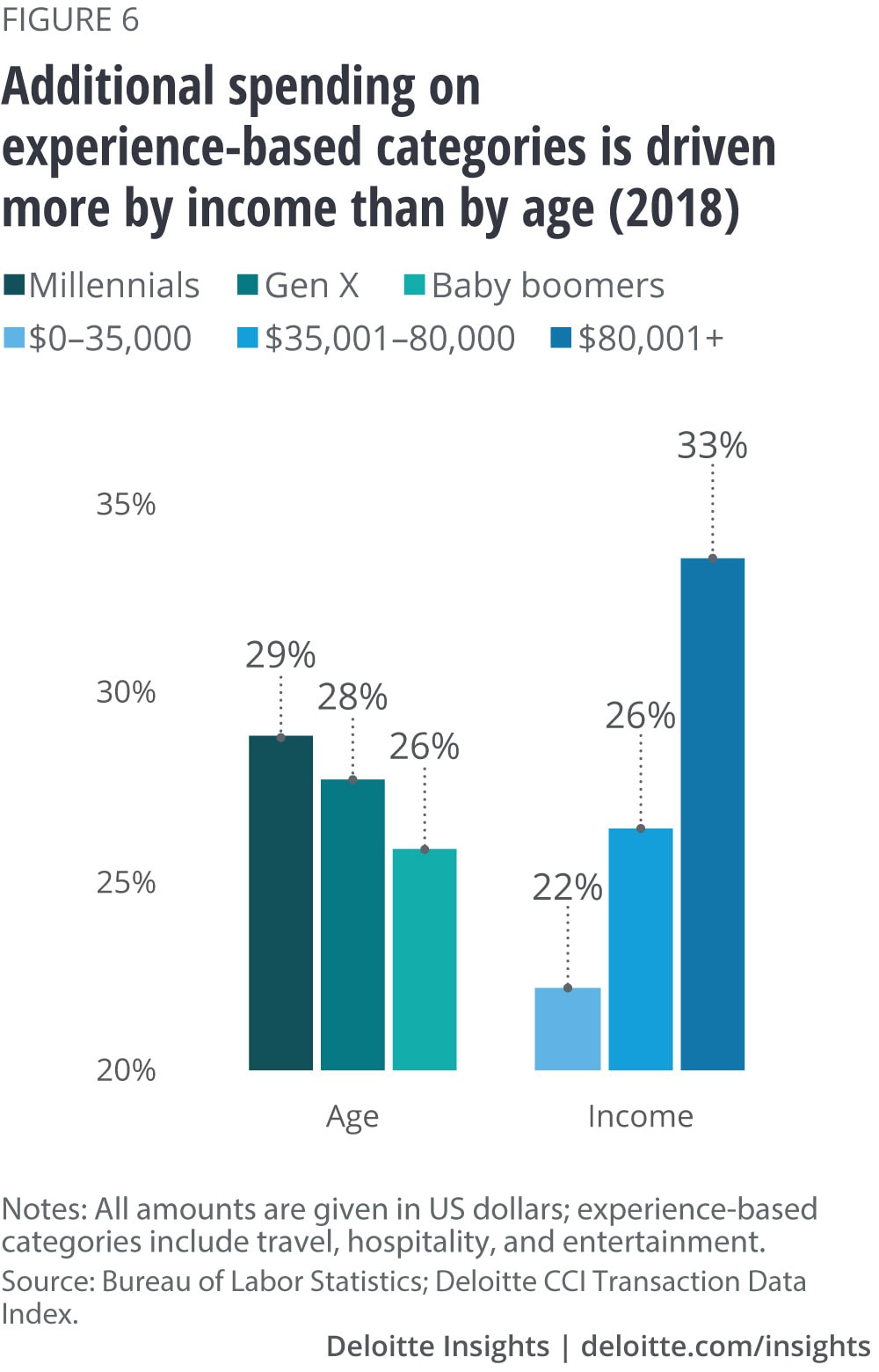

Seeing this split in millennial consumer behavior along the lines of income, we dug further to run into if the aforementioned pattern was prevalent amid other age cohorts. Indeed, increased spending on entertainment is strongly correlated to income group, much stronger than any age-related difference (effigy 6). It'due south non the younger consumer who'southward shifting toward entertainment-based spending, but rather the college-income consumer with growing discretionary spend.

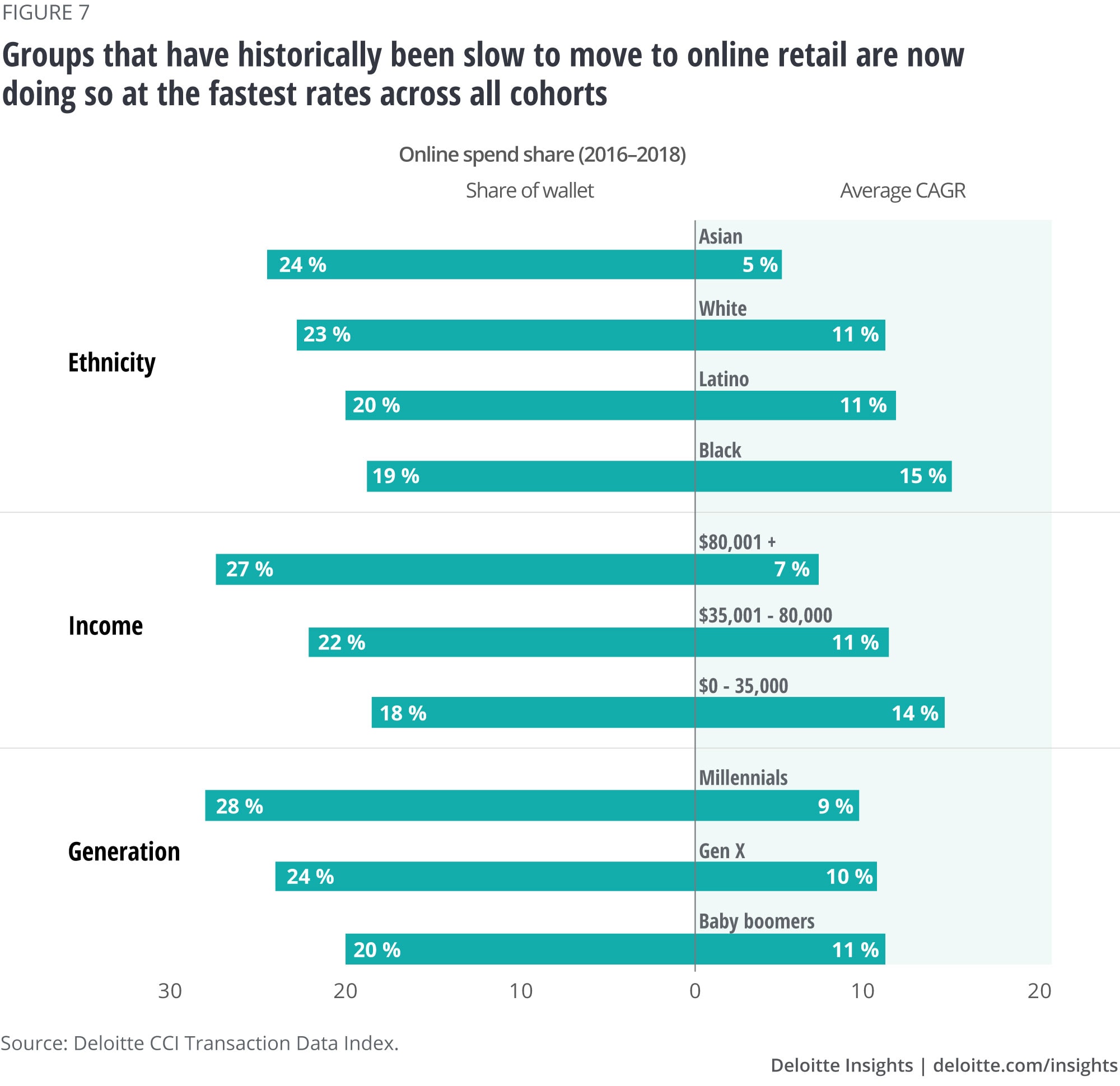

In addition to assessing spend past income and age, we challenged the existing notion effectually—who is the consumer using eastward-commerce. Eastward-commerce, which currently stands at US$517.4 billion—climbing xv percent in 201831—has grown sharply over the by decade.32 What is more interesting is how the consumer who shops through digital channels may exist changing. Not surprisingly, higher-income groups, considering they have amend access to technology, spend a larger share of their wallet online than lower-income groups—27 percent versus xix percent. The same trend is visible among millennials (28 percent) versus boomers (20 percent).

It'southward non age merely income that is driving the share of wallet allocation toward entertainment.

Still, low-income, blackness, and Hispanic groups are among the fast-growing populations in terms of online purchasing (CAGRs of fourteen.iii percentage, 14.vii pct, and eleven.v percent respectively), revealing a quickly expanding pocket of opportunity for east-commerce (figure 7).33

This growing opportunity prompted us to do a competitive review of Walmart and Amazon to see which one of these US retail behemoths is winning with these fast-growing, under-penetrated online consumer cohorts. Information technology appears that Walmart is popular among the infant boomers and the lower-income group, as it is growing its digital sales for these cohorts at 1.four times and 1.2 times the rate of Amazon, respectively. Since its acquisition of eastward-commerce retailer Jet.com, Walmart has posted a 44 percent increase in e-commerce sales, driven heavily past its current consumer base'southward increased online spending.34

Equally far every bit spending patterns are concerned, today's consumer is non so different from yesterday's buyer. United states of america retail spending has grown, but this trend has been in line with the population growth fifty-fifty equally per capita spending remains apartment. We've also seen that within specific categories—such equally food, housing, and amusement—the modify in share of wallet stayed within a tight range. That's not to say that there take been no shifts whatsoever, simply some of them—such as the declining share of wallet represented past apparel—reflect broader competitive changes in the marketplace and deflationary forces.

Where existent changes show up are in the spending patterns of different income groups—shifts that reflect the growing income bifurcation in the Us. These spending categories appear to exist having an impact on millennials, who are delaying life bike milestones—not necessarily due to a alter in values only possibly because family, children, and homeownership are out of reach financially.

Time is money. So where are consumers spending it?

It seems to be a commonly accepted truism that we are living in the age of the "time-starved consumer" who has less time than ever before. But a day is still 24 hours. That hasn't changed. So, what has?

In our survey, 76 percent of the respondents reported having less or the same amount of complimentary fourth dimension than just a year before. Our results, therefore, corroborate the broadly held view that consumers take less free time than before, at least in perception.

But here, once once again, a deeper cutting of the information tells a different story. While it is a fact that the total hours worked in the United States has risen by 43 percent since 1980, the increment has been driven by the growth of the workforce. When we cistron in the increased working-age population and labor force participation over the years, the average hours worked per person has fallen past 9 percent since 1960, which means people are spending less time working.35

Co-ordinate to the Deloitte Consumer Change Study 2018, the time not spent at piece of work is simply beingness partially redirected toward other nondiscretionary activities, such as personal intendance and household-related events, which rose thirteen percent and viii percent, respectively. In fact, the corporeality of time spent on leisure by the average consumer has risen. Bachelor discretionary fourth dimension is up overall, with fourth dimension spent on leisure and sports increasing 5 percent between 2007–2017, or an additional fourteen minutes daily, despite what consumers may be feeling.

Co-ordinate to OECD and Federal Reserve Banking concern of St. Louis data, there has been a 9 percent decrease in hours worked per person since 1960.

1 activity to which consumers have not been devoting as much fourth dimension every bit in the past is shopping. According to the The states Census Bureau, 2017, the number of minutes spent shopping has fallen by i-fifth over the by xiii years. The boilerplate consumer is spending 20 pct fewer minutes shopping every week.36 Information technology's natural to assume that the decline is likely a upshot of growing disinterest in shopping, but this assumption fails to business relationship for an important difference—the multitude of shopping channels available. Today, more than ever earlier, consumers take more efficient ways of shopping, so this decline may not really reflect a disinterest in shopping itself.

This decline in fourth dimension spent shopping is accompanied by data that shows certain cohorts—such as rural, male, and high-income consumers—are shopping at fewer places equally compared to 2017.37 As a effect, the minutes spent by consumers shopping have become increasingly valuable to retailers.

Then, a data-backed analysis of how the consumer is spending their time shows that contrary to the popular perception of the stressed and harried consumer, the reality is that people today have more discretionary time than ever before. What appears to exist happening is that the consumer is not able to relax during the increased discretionary time every bit having to choose between the options competing for that free time is exhausting!

Where are consumers going these days?

There's another conventional wisdom prevalent about the consumer—that greater adoption of digital is resulting in fewer retail-oriented trips. However, an in-depth review of location and traffic information revealed that in 2018, consumers went more than places and made more trips than they did the previous year, with consumer-oriented traffic (retail, convenience, and hospitality/travel) increasing by six percent in April–December 2017 vs. April–December 2018.

Trips to hospitality, travel, and entertainment destinations rose by 8 per centum in 2018. Trips to convenience, quick service restaurants (QSR), and fuel stations jumped sixteen percent. Even brick-and-mortar retail saw a ii percent increase in traffic. The biggest gains were seen in grocery-related trips, which grew seven.7 per centum in 2018, with a notable decrease in visits to traditional retail locations such as wearing apparel stores (i.seven percent) and department stores (10.3 percent).38

Only these changes don't consistently play out across all cohorts, with the gap nearly apparent across income groups. For example, the information reveals that the mix of trips by high-income consumers is skewed 2.four percent more than toward hospitality, travel, and entertainment than the low-income grouping.

More than importantly, gains and losses in shopping trips are concentrated amidst a fraction of the 259,000-plus stores in the United States, with 22 percent of the stores accounting for 90 percent of the gains, and 16 percent stores responsible for 90 percent of the lost trips.

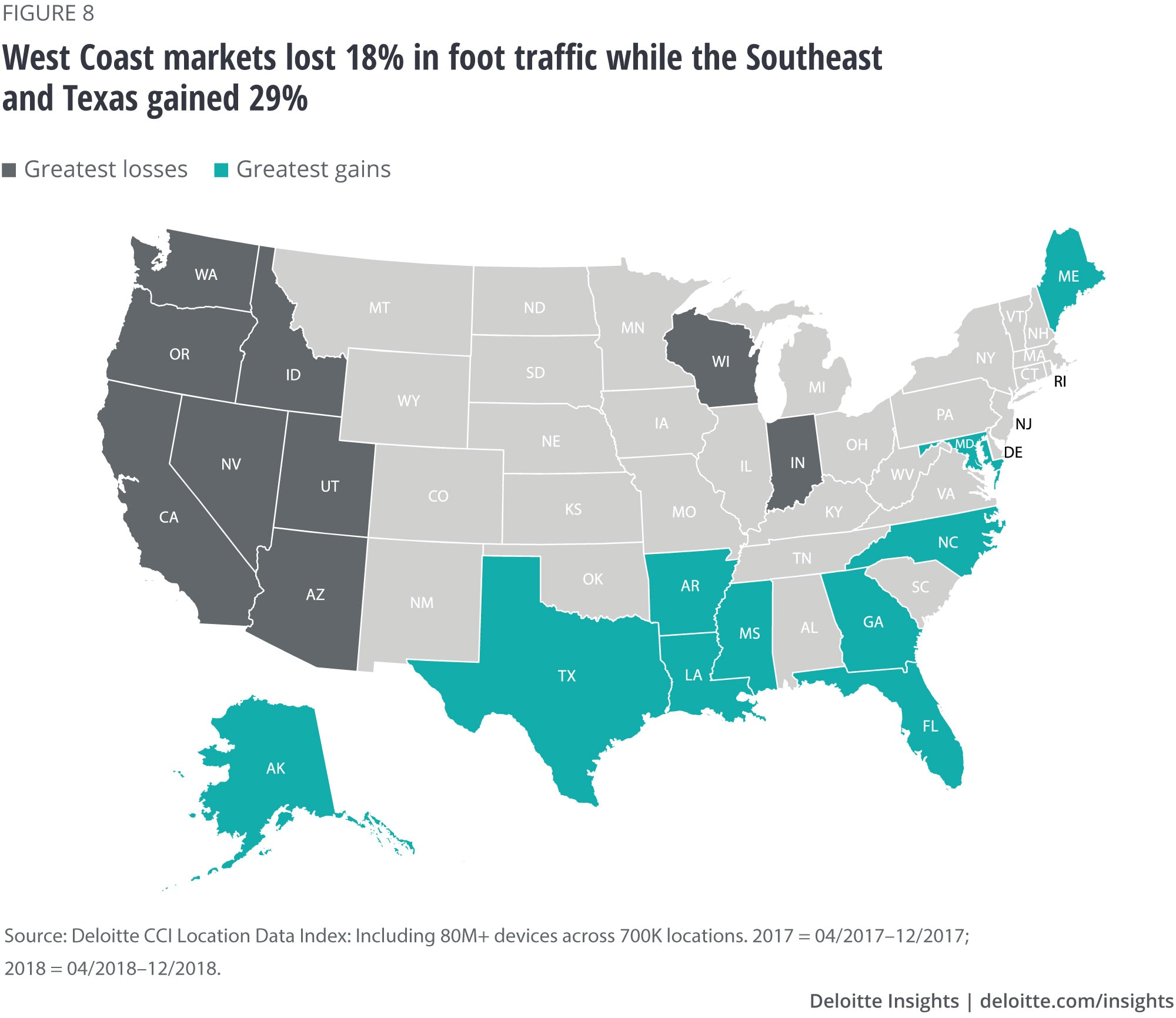

Additionally, the trends related to traffic are not homogeneous by market. The markets hitting hardest past declining traffic are also highly consolidated, with the xv fastest-declining markets largely centering around Due west Coast urban centers and the xv fastest-gaining markets centered in the Southeast and Texas (figure 8). Further, and maybe not surprisingly, eastward-commerce penetration in those geographies is highly correlated with a subtract in pes traffic. The West Coast Markets had an average e-commerce penetration of 25 percent while the Southeast and Texas (where foot traffic growth was strongest) had an average e-commerce penetration of xx percent. 39

On-mall shopping is on the decline (-7.6 pct) while off-mall shopping is upwardly (+0.5 pct). But while conventional wisdom holds that shoppers are shifting their trips away from malls, this is only half the story. What our location data revealed is that this shift away from malls is happening fastest and nearly dramatically among the older and college-income cohorts—groups that have traditionally been the core shopper in malls.xl

In that location is a myth that the new-age consumer never leaves their business firm: They're glued to their devices, ordering personal digital assistants to do everything from shopping to shutting off the lights. According to this narrative, just experiential-oriented retail tin become them off their sofas. While there is some truth in the notion that the consumer is going out less, information technology needs to be viewed through the lens of income. So nosotros see that the high-income cohort is going on more "fun" outings, such every bit hospitality, travel, and entertainment, and the lower-income grouping is going out less, relatively.

However, it'due south of import to not let the high-income cohort skew the entire story. When we investigate where consumers are going, we see they're going more than places and leaving the house more often—non less equally assumed.

What matters to consumers?

Changing consumer values have garnered a great deal of attending in recent years. Much has been said and written virtually how consumers seem increasingly focused on where products are sourced from, child labor in production development, supply chain transparency, sustainability, and other ethical matters. In that location's besides a view that consumers are increasingly drawn to products that are personalized. But are these factors determining their decision-making process?

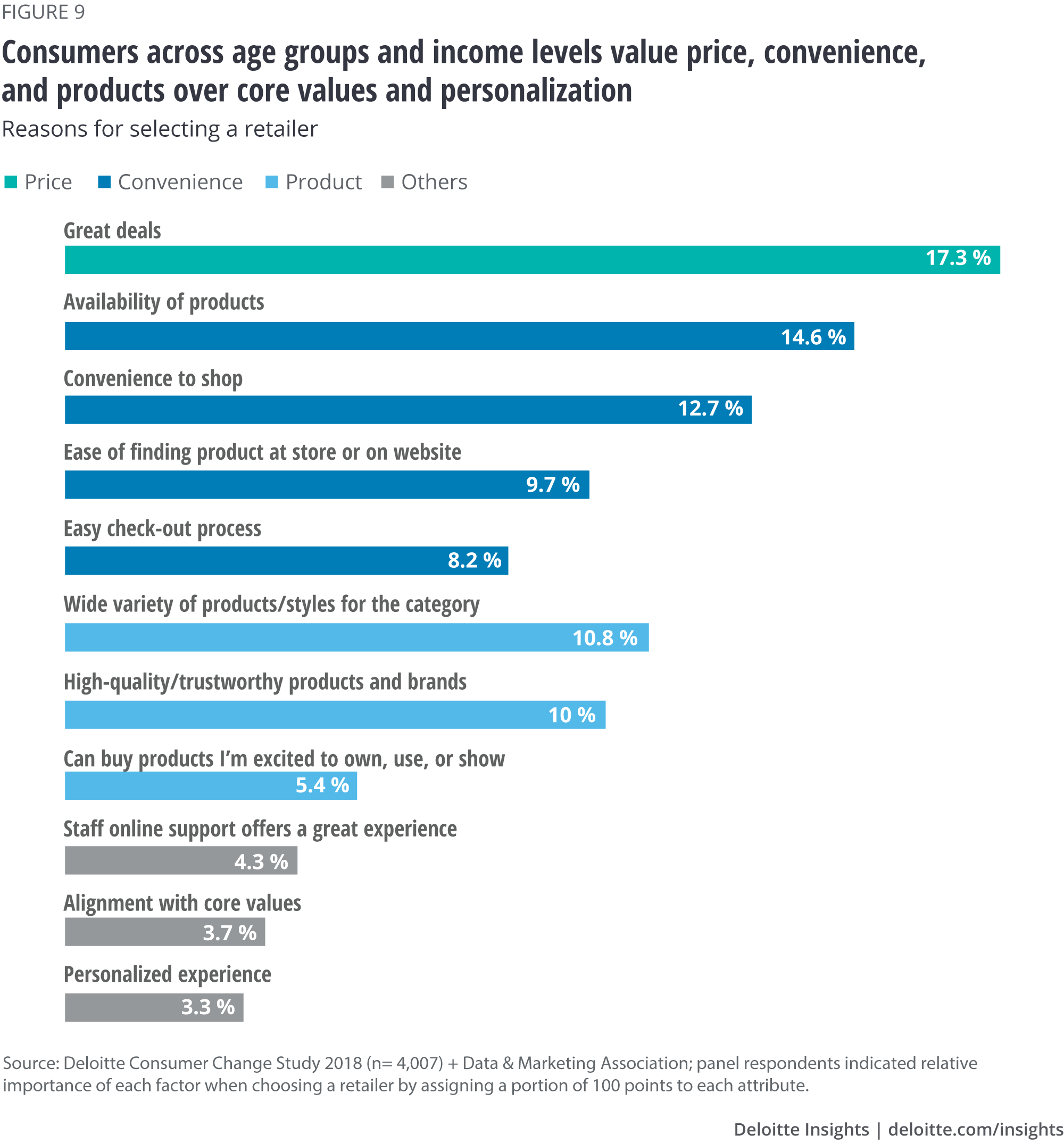

To this terminate, the survey helped the states understand the changing consumer value gear up. We found that consumers still wait to value, product, and convenience equally the overwhelmingly of import attributes while making decisions (figure 9). This finding is in line with the values that accept been held by generations of US consumers.

In fact, ofttimes-noted attributes of the modern consumer like core values and personalized experiences ranked lowest among their priorities. While this finding doesn't discount that some marginal attributes may take grown over fourth dimension, the central attributes that the consumer looks to today are similar to what we would take seen 50 years ago.

This preference holds true no thing how nosotros slice the data—along the lines of historic period or income. Consumers across the board prioritize price, product, and convenience the almost while evaluating purchasing options while alignment with core values and personalization affair the least in their retail experience. Even high-income millennials, who may exist the outliers, follow this trend.

While what matters to consumers may not accept changed significantly, we must think that the market place today is a competitive battlefield. What is convenient or what offers value is relative, and hence these parameters are likely constantly changing in the mind of the consumer.

Consumers: The more they modify, the more they remain the aforementioned

An analysis of the data and trends across demographics and consumer behavior brings to the surface a nuanced reality: The consumer is changing, but not necessarily in the ways we usually hear or think of.

The consumer is irresolute because the environment effectually them is evolving. If retailers and consumer product companies want to cater finer to changing consumer needs and identify new pockets of opportunity, it is imperative for them to empathise the demographic, economic, and competitive milieu that the consumer is reacting to.

Today's consumer is more diverse than ever along the lines of race, ethnicity, income, teaching, rural-urban divide, migration, etc. These demographic forces have led to increased fragmentation, with the and then-called "average consumer" now comprising distinct subsets of consumers who have increasingly distinct needs equally well as competitive options to address their needs.

The consumer is irresolute because of the economic constraints they are operating under—including the rising in nondiscretionary expenses such as health care and education—and the growing bifurcation between income groups, which are having an touch on spending patterns. This is especially true of the depression-income, centre-income, and millennial categories.

The changing consumer cannot be separated from the changing competitive market—they are two sides of the same coin.

However, the wallet share they spend on various categories—food, booze, furniture, food away from habitation, and housing—more or less remains constant. Also, despite the rising in online shopping, consumers are going more places than in the past.

It's important to note that the consumer can't exist viewed in isolation from the irresolute competitive market, driven by the explosion and admission to choices. The consumer is changing in reaction to the proliferation of competitive options in the market. This change has been made possible past engineering science, coupled with reduced barriers to entry, and the emergence of smaller players who are creating niche markets with more targeted offerings.

We must not misfile choice with alter. In many ways the consumer of today is like the consumer of yesterday, they are a creature of the pressures they are nether, coupled with the choices they take available to them.

0 Response to "In What Ways Has Increased Availability of Leisure Time Affected the Fashion Market?"

Post a Comment